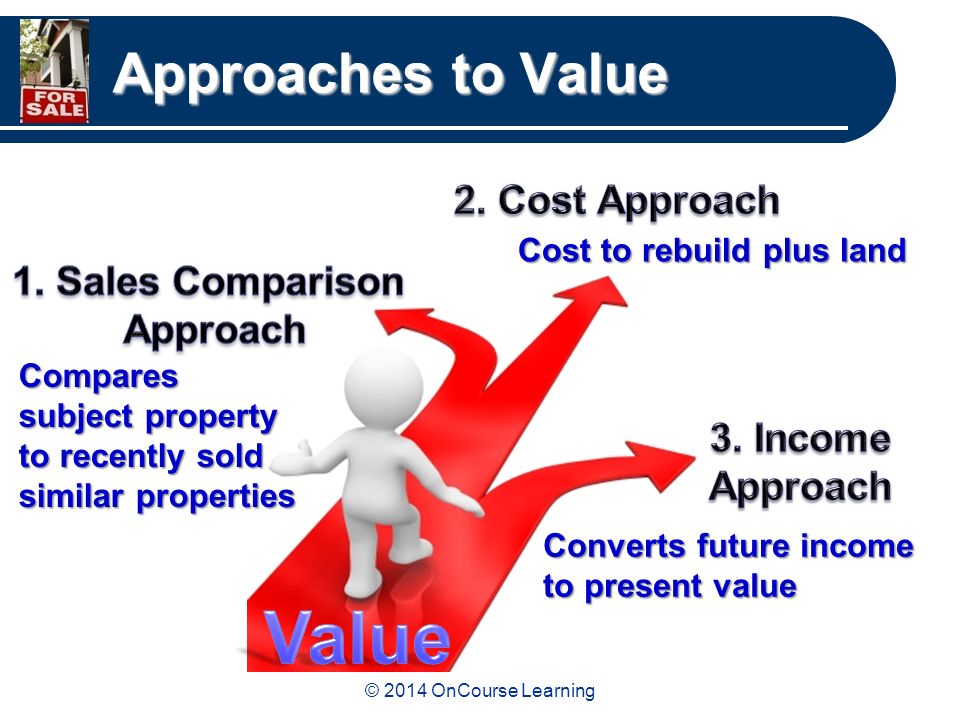

What Are the Parts of an Appraisal?A home purchase can be the largest transaction many people could ever consider. It doesn't matter if where you raise your family, a second vacation property or an investment, the purchase of real property is an involved financial transaction that requires multiple people working in concert to pull it all off. You're probably familiar with the parties having a role in the transaction. The real estate agent is the most known person in the exchange. Then, the bank provides the money necessary to fund the exchange. And ensuring all areas of the transaction are completed and that the title is clear to transfer from the seller to the buyer is the title company. So, who's responsible for making sure the property is worth the amount being paid? In comes the appraiser to provide an unbiased estimate of what a buyer might expect to pay — or a seller receive — for a property, where both buyer and seller are informed parties. As a licensed certified professional a HLC Property Appraisals will ensure, you as an interested party, are informed. Inspecting the subject propertyThe first responsibility at HLC Property Appraisals is to inspect the property to ascertain its true status. We must physically see aspects of the property, such as the number of bedrooms and bathrooms, the location, and so on, to ensure they indeed are present and are in the shape a reasonable buyer would expect them to be. The inspection includes a sketch of the house, ensuring the square footage is proper and conveying the layout of the property. Most importantly, the appraiser looks for any obvious features - or defects - that would affect the value of the house. Following the inspection, certain approaches are used to determining the value of the property: sales comparison approach, in the case of a rental property, an income approach and in the case of new construction, the cost approach.

Cost ApproachThis is where information is analyzed on local construction costs, the cost of labor and other elements to ascertain how much it would cost to construct a property similar to the one being appraised. The cost approach is the least used predictor of value due to it being the most unreliable based on a number of variables with the largest being the differences in Builder costs. This approach is not required to produce a creditable assignment.

Sales Comparison ApproachAppraisers get to know the neighborhoods in which they work. They innately understand the value of specific features to the homeowners of that area. Then, the appraiser researches recent sales in the neighborhood and finds properties which are 'comparable' to the home in question. By assigning a dollar value to certain items such as square footage, additional bathrooms, hardwood floors, fireplaces or view lots (just to name a few), we add or subtract from each comparable's sales price so that they are more accurately in line with the features of subject.

Once all necessary adjustments have been made, the appraiser reconciles the adjusted sales prices of all the comps and then derives an opinion of what the subject could sell for. The sales comparison approach to value is commonly given the most weight as it is a reflection of the market's reaction to a property. Valuation Using the Income ApproachIn the case of income producing properties -2-4 family dwellings for example - the appraiser uses a third approach to value. In this case, the amount of revenue the real estate produces is factored in with other rents in the area for comparable properties to give an indicator of the current value. This approach is not applicable for a single family home. Arriving at a Value ConclusionExamining the data from all approaches, the appraiser is then ready to document an estimated market value for the property at hand. Note: While the appraised value is probably the strongest indication of what a house is worth, it may not be the price at which the property closes. There are always mitigating factors such as the seller's desire to get out of the property, urgency or 'bidding wars' that may adjust an offer or listing price up or down. But the appraised value is often used as a guideline for lenders who don't want to loan a buyer more money than the property is actually worth. At the end of the day, HLC Property Appraisals will guarantee you attain the most fair and balanced property value, so you can make the most informed real estate decisions. |